For Family Offices · Hedge Funds · Institutional Allocators

A research-grounded derivatives strategy. Closed-loop Greek budgeting.

Gastaldi Quantitative is the institutional implementation of work

published in the academic literature under the Universal Statistical

Edge principle. The strategy manages exposure on regulated derivatives

venues under a closed-loop Greek-budgeting discipline. Investor capital

is never under our custody. The tear sheet and the data room are

available on request to qualifying allocators.

"We do not forecast. We balance exposure. Everything else that is

sold to retail traders — signals, technical analysis, predictions — is,

statistically, noise."

— Prof. Tommaso Gastaldi, principal

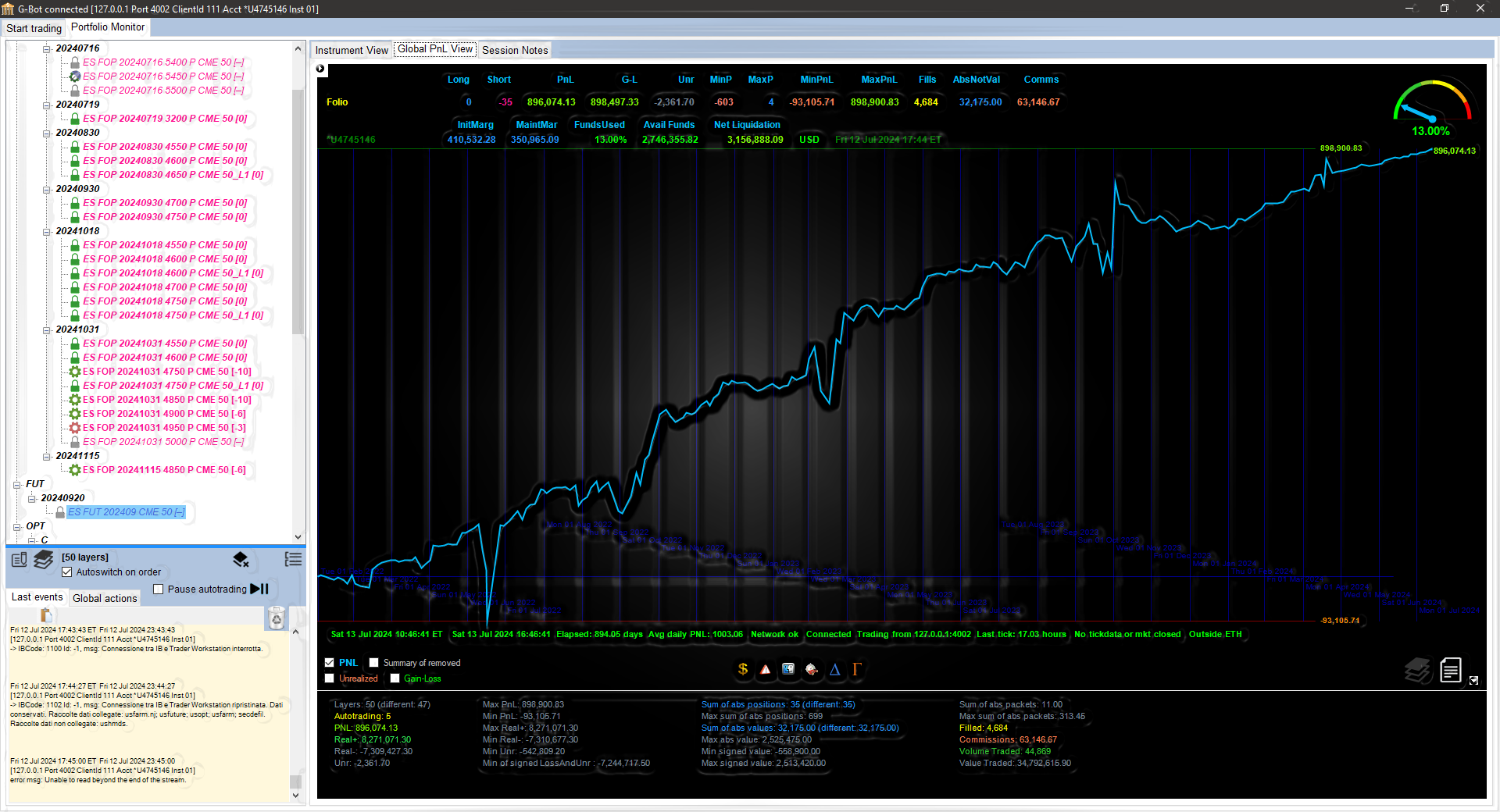

// live operator consoleportfolio · layers · folio monitor

25+

Years of methodology research

arXiv

2404.14252 — peer-visible

$0

Custody of investor capital

$700k

Capital floor · paper evaluation

// 01 · Methodology

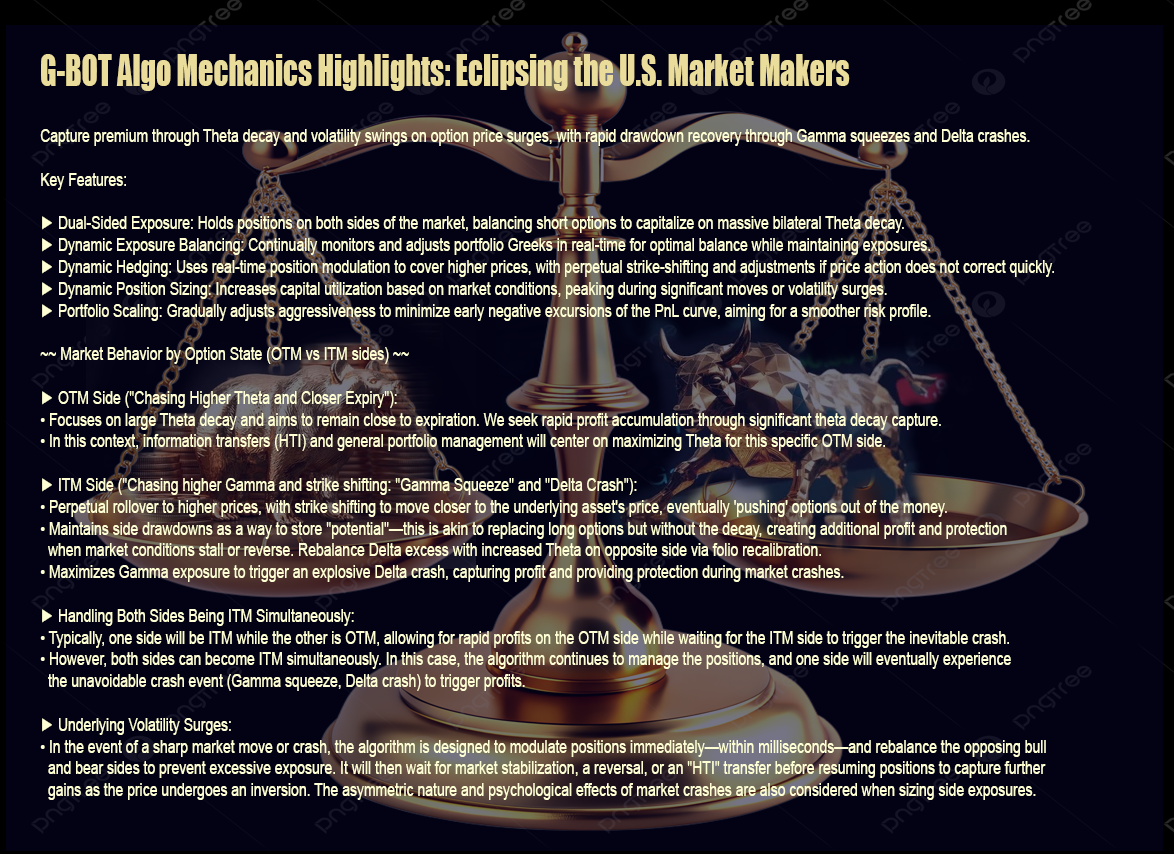

The edge is not in the chart. It is in what the book remembers.

The strategy is built on the Universal Statistical Edge

(USE) principle — the result of decades of research on what

compounds in financial markets when forecasting is removed from the

decision loop. Conventional trading lore — signals, technical analysis,

momentum — is explicitly rejected as a primary trigger.

USE Principle

Markets do not have to mean-revert. Inventory does.

The edge does not depend on the underlying reverting. It depends on

inventory cycling through harvest and reset states under an induced

price recurrence created by the bilateral book itself.

Historical Trading Information is the only durable memory.

Every fill, every stranded order, every rollover is preserved as

structured memory. The system does not predict the next tick. It

knows where every existing position came from and the conditions

that would close it profitably.

Bull and bear are coordinates in a balance, not a forecast.

The book manages bilateral inventory whose total exposure is

bounded by hard, non-bypassable Greek caps. Asymmetry is corrected

mechanically. Risk-reducing operations are never gated. New risk

is always gated. "Close-before-open" is sacred.

A one-page institutional brief. The current edition is methodology-led:

strategy, risk architecture, capital requirements. Live performance

statistics — Sharpe, Sortino, max drawdown, Calmar — are released as

the paper evaluation programme accumulates the required observation

window.

Gastaldi Quantitative

Strategy Tear Sheet · Methodology Edition

ForProfessional & Institutional Investors

As of

Strategy

Bilateral derivatives book on regulated venues, managed under the

Universal Statistical Edge (USE) principle. The strategy does not

forecast. It manages controllable inventory recurrence through

rollover, hedge and repair operations, gated by per-Greek hard caps.

Source paper: arXiv:2404.14252.

Risk architecture

Per-Greek hard caps — Δ̄, Γ, V, Θ each have non-bypassable budgets; new risk blocked at cap.

Pre-fill filter set — crossed, stale, wide-spread and thin-book quotes refused before execution.

Margin headroom buffer — bounded against the venue's worst-case stress matrix at startup.

Operator-in-the-loop — per-layer Manual/Auto switch; no autonomous flatten of the entire book.

Performance

Net annualised return

Reporting from Q1 2027

Sharpe (excess)

—

Sortino

—

Max drawdown

—

Calmar

—

Observation window

Paper evaluation in progress

Performance fields are released only after the live paper-trade

programme reaches a statistically significant window. We do not

publish back-test numbers.

We do not try to be clever about the future. We try to be disciplined

about what we already hold. The same set of ideas recurs whether the

book is one instrument or fifty.

01

No signals. No forecasts. No technical analysis.

Every chart pattern, every indicator, every momentum read is

rejected as a primary trigger. Trackers such as the Kaufman SDX

appear only as veto gates, never as buy or sell triggers.

02

Inventory as a controllable price loop.

Each instrument is a Layer. Each Layer contains Players — units

of inventory with a side, an average entry and a lineage. The system

opens, hedges, repairs and rolls Players to harvest the decay and

reset cycle.

03

Rollover is information transfer, not exit.

When a Player rolls, the Historical Trading Information transfers

to the new leg. The price loop does not depend on the underlying

actually mean-reverting — it depends on a controllable recurrence

built from the book's own state.

04

Hard caps are non-bypassable.

Greek budgets, exposure caps and margin fractions block new risk

unconditionally. Closes, forced flatten and risk-reducing hedges are

always allowed. "Close-before-open" is the operating axiom.

05

Filters before fills.

Crossed quotes, stale quotes, out-of-line bid or ask, thin

top-of-book sizes — all of them are refused. The filter set is the

single most rewritten part of the codebase. The defaults are

paranoid by design.

06

Operator-in-the-loop is mandatory.

Every Layer has a Manual / Auto switch. Every order is visible in

the order book before fill. There is no "flatten the whole folio"

button by design — if you need to flatten, you flatten Layer by

Layer while watching each fill.

07

Capital is part of the strategy.

The system is engineered to scale — single accounts up to

roughly USD 500 million, multi-account architectures beyond. Under

the capital floor, the system will not generate meaningful work.

This is the only honest answer.

08

Volatility is opportunity, not threat.

The largest absolute profits arise from movement, not calm. Quiet

markets produce few opens by design. Active markets produce the most

information — if filters and caps are respected.

// 04 · Architecture

How a mandate actually runs.

The strategy runs on the investor's own infrastructure or on a

dedicated trading workstation under our operation. It talks to the

prime broker over a single user-defined encrypted port. Investor

capital never moves under our control.

No custody. No co-mingling.

The execution engine communicates directly with the venue's

gateway over an encrypted link. Tick data, Greeks, fills, rejections

and margin events flow on that link and nowhere else. Capital

remains in the investor's own prime brokerage account at all times.

This is an architectural choice, not a compliance frill:

what is not collected cannot be betrayed. What is not stored

cannot be disclosed.

Pseudonymity is permitted during evaluation.

During the paper evaluation phase, allocators may engage under a

pseudonym. Identity disclosure is required only at the live

mandate stage.

// architecture · prime gateway · HTI loop

Stage 1 · Paper evaluation

Live tick data. Fictitious funds. Zero risk to the allocator.

You evaluate the strategy on a Portfolio Margin paper-trading

account using live exchange data. Every fill, every Greek, every

cap event is observable. There is no obligation to move to a live

mandate and no time limit on this stage.

Stage 2 · Live mandate

Same software. Same console. Investor's capital. Investor's prime.

Once you have verified forward behaviour with your own eyes, the

execution engine is repointed at a live account. Nothing is

installed on our side. Capital stays in your prime brokerage account.

Custody never transfers.

Stage 3 · Scale

Multi-account architecture from a single operator console.

Single instances cap at approximately USD 500 million for clean

risk segmentation. Beyond that, multiple instances run against

separate sub-accounts from one console — designed for family

offices and multi-mandate allocators.

Capital floor · honest answer

Minimum USD 700,000. Optimal from USD 3 million.

The instruments the strategy trades require adequate capital to

keep Greek budgets, exposure caps and margin headroom in healthy

territory. Under the floor, the system simply will not generate

meaningful work. This is the answer, not a marketing position.

// 05 · Transparency

Don't take our word for it. Watch it run.

We do not publish back-tests — back-tests are tuneable. We publish

live operator sessions, and we hand qualifying allocators the

executable so the strategy can be observed on their own console.

Forward performance, on your screen, is the only number that matters.

Recorded sessions

Forward sessions on YouTube

Annotated operator sessions, including drawdown moments, fills,

repairs and rollovers. Loss windows are not edited out.

Principal of Gastaldi Quantitative and author of the Universal

Statistical Edge principle. A long-standing presence in the

academic literature on quantitative finance, Prof. Gastaldi has

been a guest commentator on Italian prime-time television

(Anno Zero, Michele Santoro) and publishes both the

academic and the operator-facing material of this initiative under

his own name.

arXiv 2404.14252 · ResearchGate · Business Reporter · datatime.eu

// 07 · For allocators

Three doors. One data room behind them.

The qualifying conversation differs by allocator type. The data room

is the same; what we ask of you, and what you ask of us, is not.

The data room contains the methodology brief, risk-architecture

documentation, recorded operator sessions, and the paper-evaluation

packet. It is shared on a per-allocator basis. We respond directly,

by email, within two business days.

By submitting, you confirm that you are acting in a professional

capacity for an institutional, family-office, or qualifying

professional-investor mandate. We do not engage retail enquiries

via this channel.

The long-form archive. The pieces below are where the operator voice

comes through most directly — the best way to decide whether the

methodology fits how your committee thinks about derivatives mandates.

From private initiative to publicly traded company.

This is not an offer or a solicitation. It is a statement of intent.

The long-term path of Gastaldi Quantitative is a transition into a

publicly traded company in partnership with a major financial

institution with substantive expertise in the IPO process. Early

participants in the private stage have a documented path into that

transition.

We are in active conversation with prospective Strategic Sponsors

— allocators with the expertise and relationships to lead a

transition of this kind. If you recognise yourself in that

description, we invite a direct conversation.